Are you ready for the Big Squeeze?

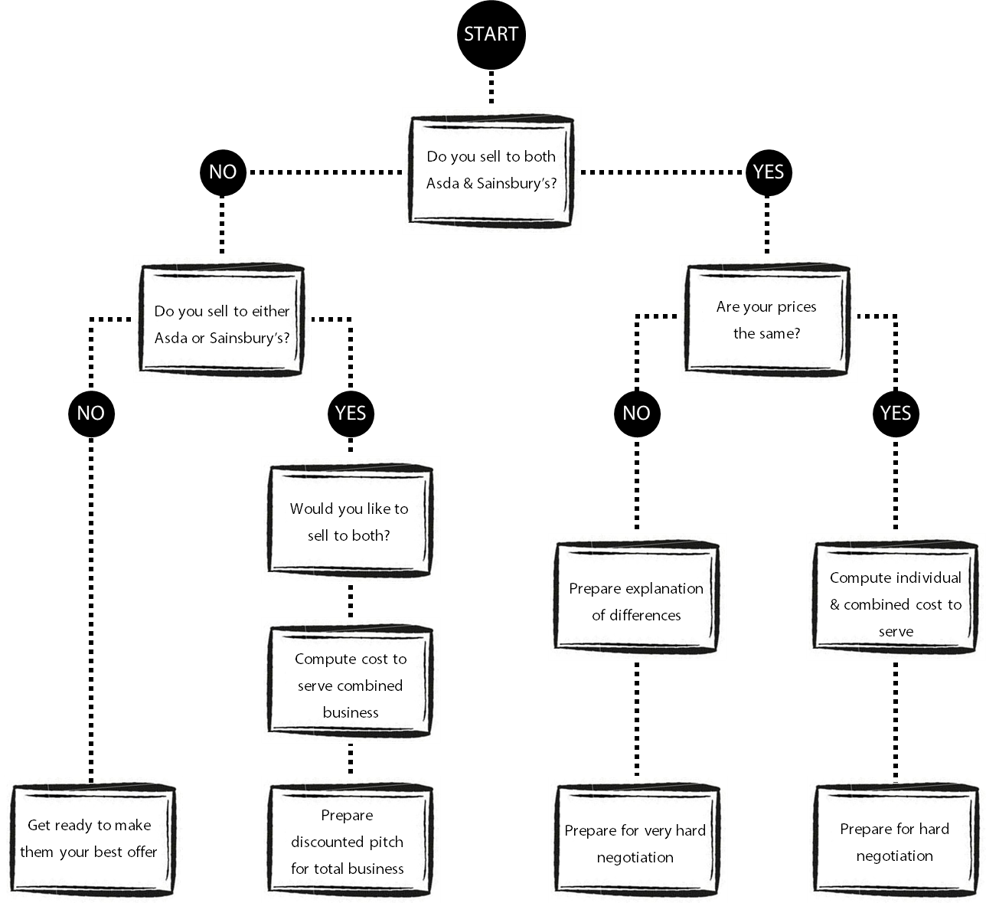

Readiness Quick Check

Sequoia’s Steve Wall chats to Martin White:

Martin, what do you think are the implications of the Sainsbury Asda merger for suppliers?

Well the first thing to note is that this is still a proposed merger, it will rumble on for many months once the inevitable Competition and Markets Authority review grinds into action. That window presents an opportunity, an opportunity to get fit for what almost certainly will come down the tracks at the conclusion of the process. The only alternative is to sit on your hands and hope that the CMA makes the whole thing go away, and precedent really doesn’t sit on the side of that one.

Why "get fit?" Well that again is looking at the inevitable – if they are going to continue to trade both facias and minimise store closures (rather than forced store disposals), then savings to fund this are mainly going to come from suppliers, there isn’t enough central overhead to deliver the aspirations being alluded to. The commitment to a 10 per cent price benefit on "products customers buy regularly", which might seem gloriously optimistic, has become the cornerstone figure of the whole deal, one that sticks in everyone’s mind to the degree that it will be how the success or failure of the enterprise will eventually be judged.

And before anyone feels this is just about grocery products, this has just as significant implications for suppliers in the apparel and general merchandise sectors too.

What in your experience has been the result of such tie ups on suppliers in the past?

There are some precedents, the recent Tesco Booker tie up, and going back the Morrisons acquisition of Safeway in 2004.

On Tesco Booker, I think we have to be careful on the parallels. At face value, it might seem that way. There are some differences to recognise however - the Booker merger is not one of a straight like for like business. there are synergies, but Booker is a business dependent on a few specific consumer products sectors, catering suppliers for example where even if there is supplier overlap, the different pack configurations reduce the synergy level. the biggest overlap will be in the core branded convenience categories - tobacco, soft drinks, confectionery, snacks and BWS - those are the areas where buying overlaps are likely to be exploited the most.

As for Safeway Morrisons, well that was a difficult union that leaked a significant amount of market share before integration was complete and a trading recovery began. That perhaps reduced the hit to the supplier community but there was own label rationalisation and renegotiation of terms that rippled through the sector.

Unlike then, these are not two embattled grocers seeking shelter in a storm, these are major scale players looking to sustain and exploit their respective market positions to limit the effectiveness of Tesco's recovery, the growth of the Continental Discounters, and halt Primark's inexorable march in the value fashion space.

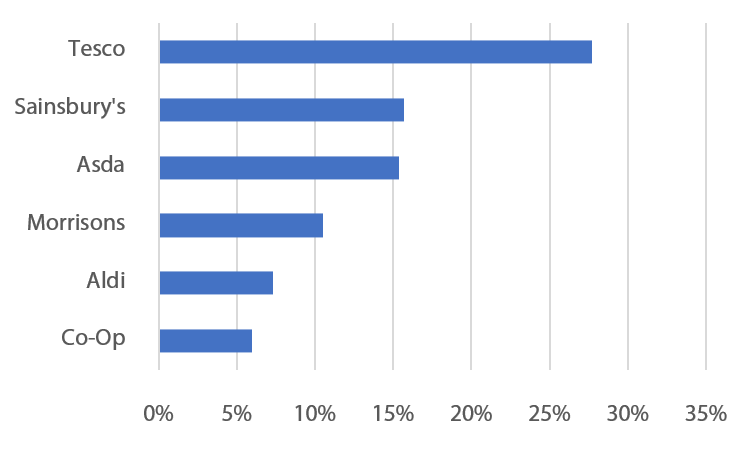

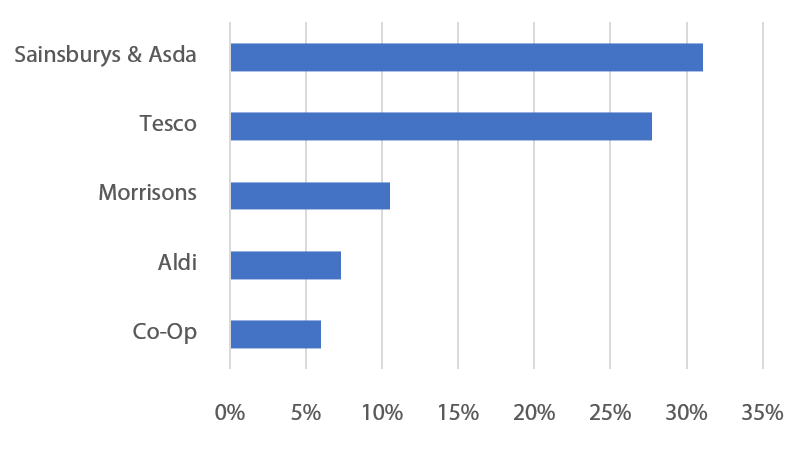

Share of the market

Pre-merger

Post-merger

What can suppliers do to protect their interests?

Its all about really understanding your current position and then building a robust set of plans from there

The first part is to understand the degree of any exposure to pressure

- Price file comparison – the obvious matching of terms to the two retailers, including discount structures, volume arrangements, marketing monies etc. This is the most urgent task to gain a base line

- Other terms – activities that make up the overall cost to serve – order costs, full truck or full pallet deals, merchandising support and so on

Then it is about the "what ifs"

- If distribution networks are merged, what could change in your cost to serve?

- Is there a private label decision and what is economically viable? Is having both retailers’ own brand feasible, and at what price? Alternatively, if own label volume goes elsewhere, what are the consequences?

This is all about developing a plan that looks at what synergies or cost savings can be engineered, what they are worth in each instance and how they can be turned into a negotiating strategy. Such a plan must be comprehensive and cover every touch point – sales, marketing, customer service, manufacturing and logistics.

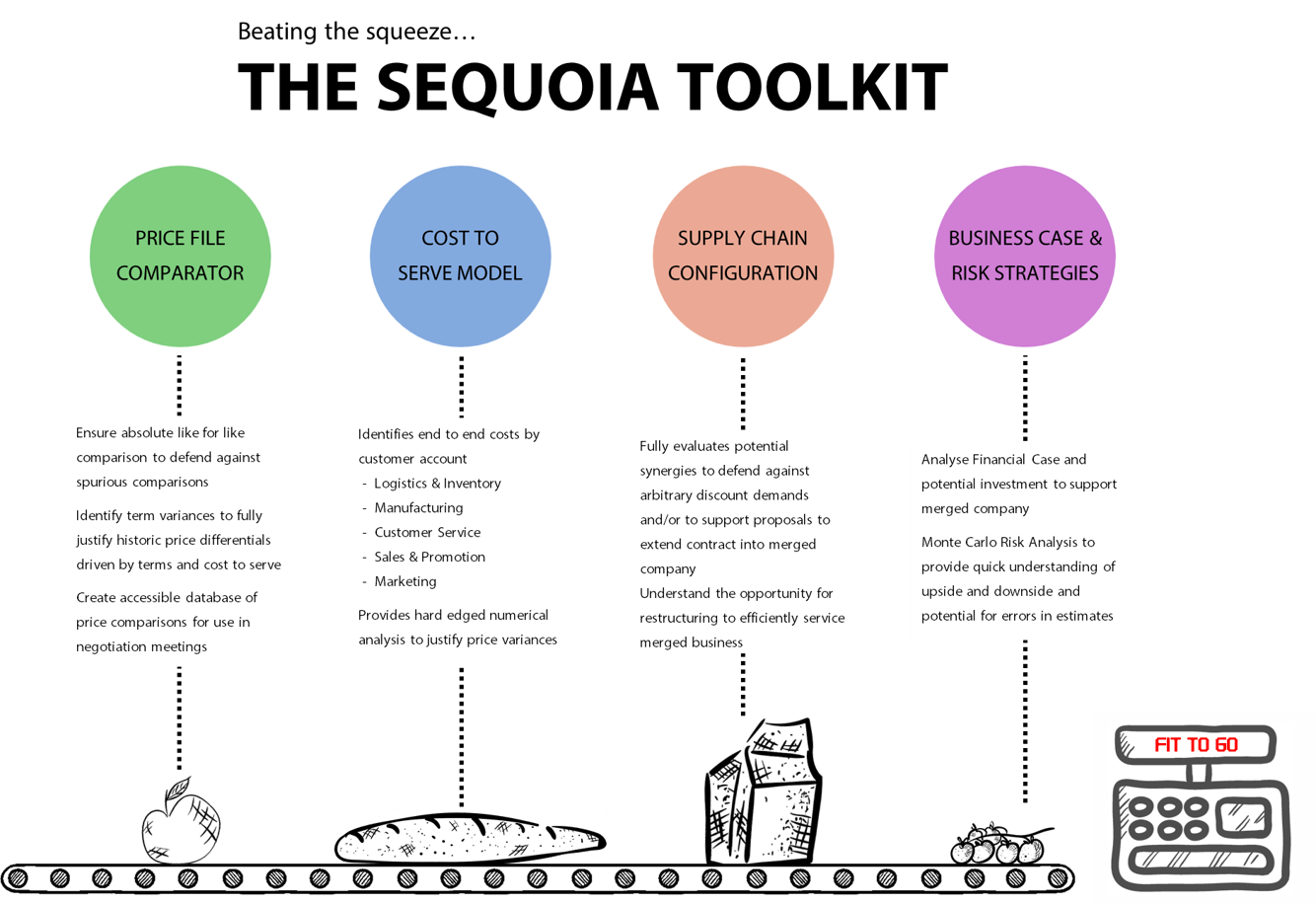

Can Sequoia help your clients to be ready for this?

Yes. At Sequoia we have developed a toolkit based on our experience from working across the consumer goods supply chain to help businesses think through the implications and build appropriate fact-based strategies. Our retail insight is matched with deep analytical understanding of end to end supply chain processes and costs, and of course we would love to come and discuss our thoughts with you.

Steve Wall is a Consumer Goods supply chain expert working for over 30 years with manufacturers…

Martin White has been a chief supply chain officer leading wholesale, retail grocery and retail apparel operations and has been involved in some of the previous sector merger deals

More than 50 years of experience:

After a career in Unilever and Coopers & Lybrand (now PWC) Steve Wall founded Sequoia over 25 years ago. Steve has worked with most major FMCG manufacturers and UK retailers at a senior level, advising on Supply Chain strategy and optimisation of operations. LinkedIn

After a career at Cooper & Lybrand Martin White has been a Chief Supply Chain Officer at Booker, J Sainsbury and Primark for over 20 years in total. Martin has been involved in many major sector merger deals – both as a Director and as an advisor.

?

?